Truck Insurance Coverage Explained

Truck insurance coverage only makes sense when the language is understood correctly.

In trucking, coverage confusion doesn’t come from complexity alone. It comes from reused terms that behave differently depending on who controls the truck, how it operates, and where responsibility sits. Liability, physical damage, cargo, and downtime coverage are often discussed as fixed protections.

ruck insurance coverage is often misunderstood because terms change meaning by operation. Learn how trucking insurance coverage works, how coverage types interact, and how responsibility shapes protection.

It functions within the broader commercial insurance ecosystem used across regulated industries.

ruck insurance coverage is often misunderstood because terms change meaning by operation. Learn how trucking insurance coverage works, how coverage types interact, and how responsibility shapes protection.

It functions within the broader commercial insurance ecosystem used across regulated industries.

Truck insurance coverage is often misunderstood because terms change meaning by operation. Learn how trucking insurance coverage works, how coverage types interact, and how responsibility shapes protection.

It functions within the broader commercial insurance ecosystem used across regulated industries.

This page explains truck insurance coverage as it actually works in real trucking operations — not as policy names, but as coverage behaviors shaped by responsibility and exposure.

What “Coverage” Means in Truck Insurance

In trucking, coverage does not mean what is listed on a declarations page.

Coverage means how insurance responds when loss occurs.

A coverage may exist and still fail to respond if:

Responsibility is misunderstood

Operational control is assumed incorrectly

The coverage triggers under conditions different than expected

This is why trucking insurance coverage must be understood structurally, not nominally.

Why Truck Insurance Coverage Is Commonly Misunderstood

Truck insurance coverage is misunderstood for three systemic reasons.

Reused Terminology Across Different Operations

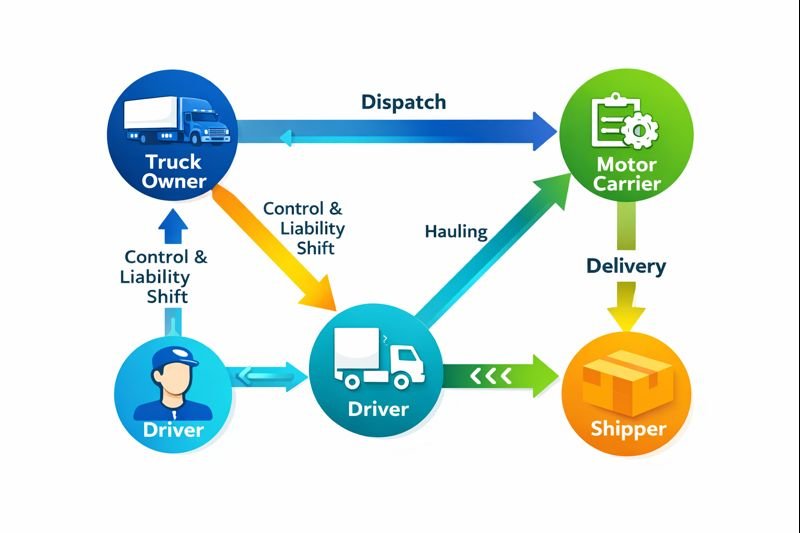

The same coverage term can apply differently to owner-operators, leased drivers, and fleets — even when the policy name is identical.

Coverage That Depends on Control, Not Ownership

Many trucking insurance coverages respond based on who controls the truck at the moment of loss, not who owns it or pays the premium.

Coverage That Interacts With Other Coverage

Truck insurance coverage works as a system. One layer often assumes another exists, and confusion arises when those assumptions fail.

The Only Coverage Categories That Exist in Truck Insurance

All trucking insurance coverage falls into five functional categories.

Everything else is a variation.

- Third-Party Liability Coverage

Responds when truck operation causes injury or property damage to others.

- Vehicle & Equipment Protection

Addresses damage to the truck or attached equipment.

- Cargo Responsibility Coverage

Responds when freight is damaged, lost, or stolen.

- Income & Downtime Protection

Addresses lost revenue when a truck cannot operate.

- Operational Gap & Transitional Coverage

Handles exposure during non-standard operating phases.

Understanding these categories prevents coverage confusion across the site.

Liability Coverage: The Foundation Layer

Liability coverage is the base of all truck insurance coverage.

It responds when:

The truck causes bodily injury or property damage

The truck is under active operational control

Coverage behavior depends on:

Operating authority

Lease structure

Control at the time of loss

Most coverage disputes begin with misunderstandings at this layer.

Physical Damage Coverage: Protecting the Truck Itself

Physical damage coverage addresses damage to the truck.

Its relevance depends on:

Who absorbs financial loss when the truck is damaged

Whether downtime affects revenue

How the truck is contractually obligated

Ownership alone does not define exposure.

Cargo Coverage: Responsibility vs Possession

Cargo coverage responds when freight is damaged or lost.

Key determinants:

Contractual responsibility

Control over transport

Carrier vs intermediary role

Possession of cargo does not always equal responsibility.

Downtime & Income Interruption Coverage

Downtime coverage addresses lost income when a truck cannot operate.

These coverages vary widely in:

Trigger conditions

Duration

Exclusions

Assumptions often exceed actual protection.

Operational Gap Coverage

Some coverage exists to manage:

Transitional use

Non-driving exposure

Short-term operational gaps

These coverages are situational and context-dependent.

How Coverage Behavior Changes by Operation Type

Truck insurance coverage behaves differently depending on how the truck is used.

Owner-operators: centralized responsibility

Leased operators: shifting responsibility

Fleet commercial truck insurance

Interstate operations: expanded exposure

Coverage explanations without operational context are incomplete.

Coverage Interaction: Why Layers Matter

Truck insurance coverage is interdependent.

Examples:

Liability determines when cargo coverage responds

Physical damage affects downtime exposure

Control determines policy priority

Understanding interaction prevents false confidence.

Common Coverage Misunderstandings in Trucking

Repeated issues include:

Assuming coverage applies because it exists

Confusing ownership with responsibility

Treating policy names as guarantees

Ignoring operational changes

Most disputes arise from assumptions, not absence of insurance.

How to Use Coverage Language Across This Site

This page defines coverage language used throughout the site.

All other pages assume:

Operational context matters

Coverage behavior depends on control

Coverage interaction shapes outcomes

This keeps explanations consistent and accurate.

FAQs

What does truck insurance coverage mean?

It describes how insurance responds to loss based on responsibility and control, not just policy listings.

Is trucking insurance coverage the same for all operations?

No. Coverage behavior varies by operation type and control structure.

Why do coverage gaps happen even when insurance exists?

Because coverage assumptions often don’t match how the truck actually operates.

Do all trucks need the same coverage types?

No. Coverage needs depend on use, not vehicle category alone.

Can coverage behavior change over time?

Yes. Operational changes often alter how coverage responds.

Why does coverage language matter so much in trucking?

Because reused terms behave differently across operations.

Bottom Line

Truck insurance coverage is not defined by names.

It is defined by control, responsibility, and interaction.

Once coverage language is understood correctly, every other insurance topic becomes clearer.

This page is the reference point.